Best Student Loan Repayment Plan for Physicians (2026)

Choosing the best student loan repayment plan for physicians is the single most valuable financial decision most doctors make before they ever draw an attending salary — and the wrong choice can cost six figures. This guide compares every 2026 option (PSLF, the new RAP plan, capped legacy IBR, refinancing, and the standard plan) and gives you a clear, numbers-first way to pick the right one for your situation.

The short version

- There is no single best plan — it depends on your balance, income trajectory, employer type, and filing status.

- Nonprofit/government for ~10 years? PSLF is usually cheapest — tax-free forgiveness.

- High attending income and want a payment ceiling? Capped legacy IBR often beats RAP.

- Certain you won't use forgiveness? Compare refinancing against aggressive payoff.

- 2026 changed the menu — re-check against current rules and your latest numbers.

The honest answer: there is no universal "best" plan

Anyone who tells you there is one best student loan repayment plan for physicians is selling something. The right plan depends on four inputs you control: your loan balance, your income trajectory (resident today, attending tomorrow), your employer type (nonprofit/government vs. for-profit), and your filing status.

Change any one and the answer can flip. A pediatrician headed for an academic hospital and a dermatologist joining a private practice should almost never be on the same plan.

The five repayment options physicians actually choose between

1. PSLF (Public Service Loan Forgiveness)

If you work full-time for a 501(c)(3) nonprofit or government employer, PSLF forgives your remaining federal Direct Loan balance tax-free after 120 qualifying payments on an income-driven plan. For high-debt physicians who train and work at nonprofit hospitals, this is frequently the best student loan repayment plan available — the forgiveness can be worth far more than any interest saved by refinancing. New to it? Start with PSLF for doctors explained.

2. The RAP plan (Repayment Assistance Plan)

RAP is the new income-driven plan under the 2025 law, available from July 1, 2026. It sets payments at 1–10% of total income, reduces them for dependents, waives unpaid interest, and forgives the balance after 30 years. The catch for doctors: RAP has no payment cap, so as an attending your payment can climb well above what capped legacy IBR would charge.

3. Capped legacy IBR

The legacy Income-Based Repayment plan caps your monthly payment at the standard 10-year amount — a crucial protection for high earners. If you first borrowed before the 2026 cutoff and qualify, capped IBR is often the best student loan repayment plan for a physician who wants forgiveness-track flexibility and a payment ceiling once their income jumps.

4. Refinancing (private)

Refinancing swaps your federal loans for a private loan at a potentially lower rate. It is permanent and forfeits PSLF, income-driven plans, and federal protections. It is the right move only when you are certain you will not use forgiveness — typically a private-practice physician with a manageable balance. Weigh it with our should I refinance guide.

5. Standard repayment

The default 10-year plan pays the loan off fastest with the least interest, but the payments are unaffordable for most residents and it wastes PSLF-qualifying months for those on the forgiveness track.

How to choose the best student loan repayment plan for physicians

Work through these questions in order:

- Will you work for a nonprofit or government employer for ~10 years? If yes, PSLF is likely your best student loan repayment plan — stay on a qualifying income-driven plan and certify employment yearly.

- Are you unsure, or headed to private practice? Model an income-driven plan (RAP or capped IBR) now, keep your options open, and re-run the math when you sign your attending contract.

- Definitely private practice with a manageable balance and no forgiveness? Compare refinancing rates against an aggressive payoff.

- High attending income and want a payment ceiling? Capped legacy IBR usually beats RAP because of the cap — if you qualify.

The decision hinges on your real numbers, which is exactly why a free physician student loan calculator that models every path side by side beats any rule of thumb.

By career stage: residents, fellows, and attendings

Residents and fellows should get on an income-driven plan immediately. Your payments are low — sometimes $0 — and those are the cheapest PSLF-qualifying payments you will ever make. Don't sit in forbearance if you're forgiveness-track. See our resident student loan strategy guide.

New attendings face the biggest swing. The best student loan repayment plan for physicians at this stage depends entirely on whether you stayed nonprofit (finish PSLF) or moved private (compare refinance vs. payoff). Re-run the decision the week your income changes — see our new attending checklist and how PSLF works for physicians.

Dentists carry the highest debt and mostly enter private practice, so the calculus tilts toward refinancing or capped IBR more often than for MDs.

The 2026 changes you can't ignore

Under the 2025 federal law, SAVE is being wound down, RAP launches July 1, 2026, and there is a June 30, 2026 consolidation deadline for borrowers who must consolidate to reach certain income-driven plans. A new loan disbursed on or after July 1, 2026 can forfeit access to legacy plans — so when you first borrowed now shapes which "best" plan is even available to you. Confirm the current rules directly at the U.S. Department of Education's Federal Student Aid site.

Because the rules keep shifting, the best student loan repayment plan for physicians in 2026 is the one that is re-checked against the current federal rules and your latest numbers — not the one you picked in med school and forgot. If you have older loans, read the 2026 legacy-borrower trap.

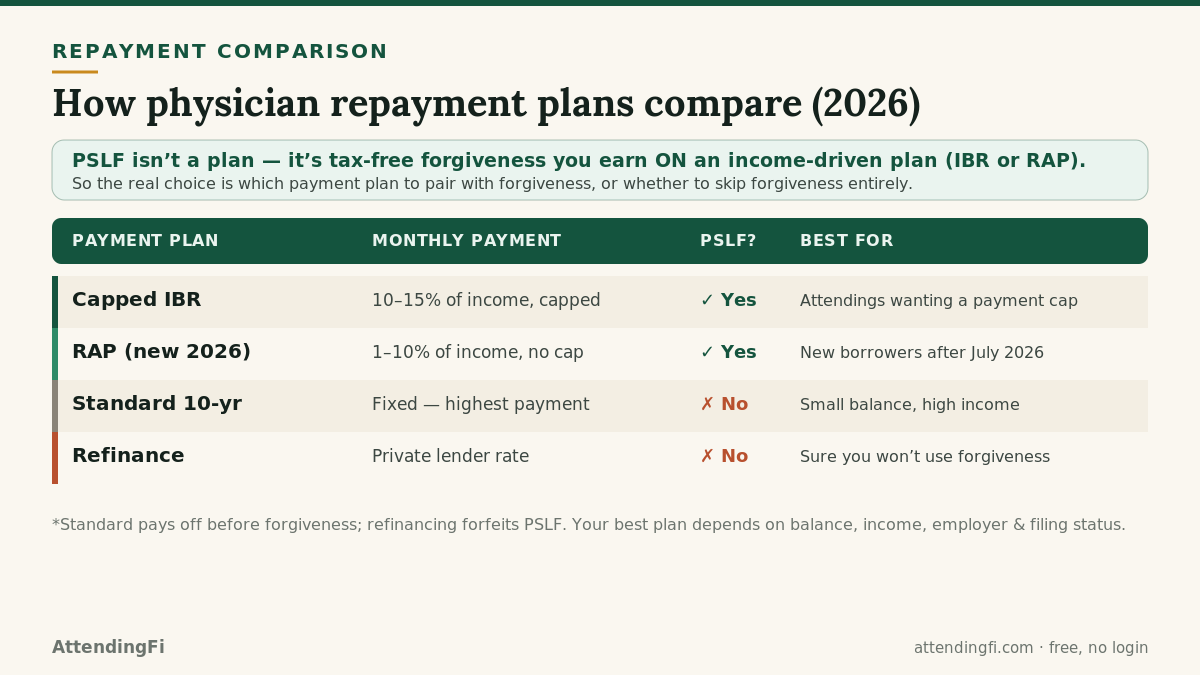

The five options at a glance

One caveat before the table: PSLF is not a repayment plan. It is tax-free forgiveness you earn on an income-driven plan (capped IBR or RAP). So the real decision is which payment plan to pair with a forgiveness strategy — or whether to skip forgiveness and pay the loan off directly.

| Path | Monthly payment | Forgiveness | Best for |

|---|---|---|---|

| Capped IBR + PSLF | 10–15% of income, capped at Standard | Tax-free at 120 payments | Nonprofit/gov attendings who want a payment ceiling |

| RAP + PSLF | 1–10% of income, no cap | Tax-free at 120 payments | New borrowers (post-July 2026) at nonprofits |

| RAP or IBR (no PSLF) | Income-driven | Taxable, at 20–30 years | Private-practice physicians who can't refinance affordably |

| Refinance | Private lender rate | None (forfeited) | Private practice, strong cash flow, no forgiveness |

| Standard 10-year | Fixed — highest | None | Small balance relative to income |

Illustrative. The exact winner is decided by your numbers — run them free in the physician student loan calculator.

Two physicians, two different "best" plans

The same rules produce opposite answers depending on the inputs. Consider two real-world archetypes.

Dr. A: academic pediatrician, $240k balance, nonprofit hospital

She trains and stays at a 501(c)(3) children's hospital. Her cheapest path is almost never to pay the loan off. On capped IBR, she makes low income-driven payments through residency and fellowship, her attending payment is capped at the Standard amount, and after 120 payments the six-figure remaining balance is forgiven tax-free. Refinancing here would be a catastrophic mistake — it would trade tax-free forgiveness for a slightly lower interest rate on a balance she was never going to fully repay. For her, the best student loan repayment plan for physicians is capped IBR paired with PSLF.

Dr. B: dermatologist, $190k balance, joining private practice

He finishes a three-year residency at a nonprofit (banking a few years of PSLF-eligible payments, just in case) and then joins a for-profit group at a high attending salary. Because his employer no longer qualifies for PSLF and his income is high, forgiveness is off the table. His fastest, cheapest route to zero is to refinance to a lower private rate and attack the principal aggressively. For him, refinancing is the best plan — the exact opposite of Dr. A, on a nearly identical starting balance.

The lesson: the "best" plan is a function of employer, balance, and income trajectory, not a universal ranking. That is why a side-by-side model beats any single rule of thumb.

RAP vs. capped IBR: the attending's dilemma

For forgiveness-track physicians, the sharpest 2026 question is RAP versus capped legacy IBR. Both keep payments income-driven and both count toward PSLF, but they diverge exactly when a physician's income jumps.

- Capped IBR caps your monthly payment at the 10-year Standard amount. Once you're an attending earning $300k+, that cap is a powerful protection — your payment stops rising even as your income does, which keeps more of your balance intact for forgiveness.

- RAP has no cap. Its 1–10% tiers can push an attending's payment well above the Standard amount, shrinking the balance that eventually gets forgiven. RAP does waive unpaid interest, which helps residents, but for a high-earning attending on the PSLF track, the missing cap usually makes it more expensive than capped IBR.

The wrinkle: capped IBR is only available if you first borrowed before the 2026 cutoff and qualify. New borrowers may only have RAP. So the honest answer to "RAP or IBR?" is: model both against your actual attending income, because eligibility — not preference — often makes the decision for you.

Common six-figure mistakes to avoid

Even the right plan can be undone by a single wrong move. The most expensive errors physicians make while choosing the best student loan repayment plan for physicians:

- Refinancing before ruling out PSLF. It's permanent and forfeits tax-free forgiveness — the single costliest mistake in medicine's financial life. Confirm forgiveness is truly off the table first.

- Overpaying a balance that's headed for forgiveness. Every extra dollar on a PSLF-bound loan is a dollar of forgiveness you gave up.

- Sitting in forbearance during residency. Those are the cheapest PSLF-qualifying months you'll ever have — skipping them wastes years of credit.

- Never certifying employment. Without the annual PSLF form, your qualifying-payment count isn't tracked, and errors surface too late to fix.

- Choosing a plan once and forgetting it. The best plan in residency is rarely the best plan as an attending. Re-run the decision at every income change.

Avoiding these five is worth more than optimizing the plan choice itself. When in doubt, model the irreversible move before you make it.

Frequently asked questions

What is the best student loan repayment plan for physicians pursuing PSLF?

An income-driven plan (capped IBR if you qualify, or RAP) that keeps your payments low and PSLF-qualifying while you complete 120 payments at a nonprofit or government employer.

Is RAP or IBR better for physicians?

For a high-earning attending, capped legacy IBR is often better because it caps your payment at the standard amount; RAP has no cap. But eligibility depends on when you first borrowed — model both.

Should physicians refinance their student loans?

Only if you're certain you won't use PSLF or federal protections. Refinancing is permanent and can be a six-figure mistake for a forgiveness-eligible doctor.

Related guides

Educational estimates, not financial, tax, or legal advice. Program rules change; verify your situation at studentaid.gov and with a qualified advisor. Model your own numbers free at AttendingFi — no login required.