PSLF for Doctors Explained: The Complete 2026 Guide

Here is PSLF for doctors explained without the jargon: Public Service Loan Forgiveness can erase your remaining federal student loans tax-free after ten years of qualifying work — and for physicians carrying $200,000+ in debt, it is often the single most valuable program available. This guide walks through exactly how it works, who qualifies, and the 2026 rule changes every doctor needs to know.

The short version

- PSLF forgives your remaining federal Direct Loan balance tax-free after 120 qualifying payments.

- You must work full-time for a government or 501(c)(3) nonprofit employer, on a qualifying income-driven plan.

- Eligibility follows your W-2 employer, not the hospital building.

- Residency and fellowship years usually count — start the clock early.

- Certify employment (ECF) every year; never refinance if you're forgiveness-track.

PSLF for doctors explained in one paragraph

PSLF forgives your remaining federal Direct Loan balance, tax-free, after you make 120 qualifying monthly payments while working full-time for a government or 501(c)(3) nonprofit employer, on a qualifying income-driven repayment plan. That's the whole program. Everything else is detail — but for physicians, the details are where six figures are won or lost.

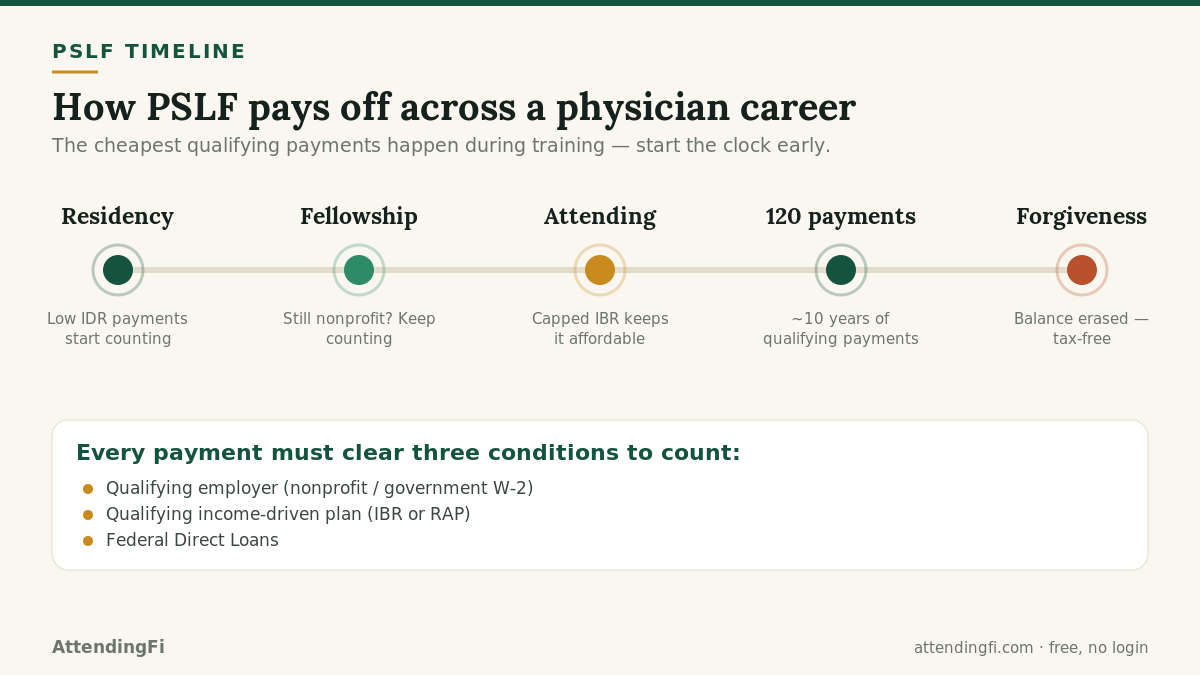

The 120-payment rule

The 120 payments don't have to be consecutive, and they don't reset if you switch qualifying jobs. What matters is that each payment is made while employed full-time by a qualifying employer, on a qualifying plan, on Direct Loans. Miss any of those three conditions and the month doesn't count.

The most valuable payments are the cheapest ones — the low, income-driven payments you make during training. That's why PSLF for doctors explained properly always starts in residency, not at attending income.

What counts as a qualifying employer

This is the trap that catches physicians. Eligibility follows your employer of record — the entity on your W-2 — not the hospital where you physically work.

- Qualifies: government agencies, the VA, public/state hospitals, and 501(c)(3) nonprofit hospitals and universities.

- Does not qualify: for-profit employers — including for-profit physician groups and staffing companies that place you inside a nonprofit hospital (common in radiology, EM, anesthesiology, pathology, and hospitalist medicine), and 1099/independent-contractor arrangements.

Always verify your specific employer using the PSLF employer search at studentaid.gov before counting on it, and re-check any time you change jobs or your group changes ownership. Our how PSLF works for physicians guide and 1099 & locum PSLF guide cover the edge cases.

Do residency and fellowship years count?

Usually yes. Most teaching hospitals, university medical centers, and VA facilities are nonprofit or government employers, so residents and fellows are often at a qualifying employer from day one — making qualifying payments at the lowest amounts of their careers.

A longer training path is an advantage here: a resident who completes a multi-year residency plus a fellowship at university hospitals can bank five, six, or more years of qualifying payments before ever earning an attending salary. See our PSLF for residents guide.

The 2026 changes to PSLF

Two developments make 2026 a year to re-check your plan:

- A new repayment landscape. SAVE is being wound down and the new RAP plan launches July 1, 2026, with a June 30, 2026 consolidation deadline for borrowers who must consolidate to reach certain income-driven plans. Because your repayment plan is what keeps payments PSLF-qualifying, these changes touch PSLF directly — see the 2026 student loan changes for physicians.

- A new employer-eligibility rule. Effective July 1, 2026, the Department of Education can disqualify an otherwise-qualifying employer found to have a "substantial illegal purpose." The Department estimated this affects only a very small number of employers nationwide, so for physicians at major academic and public systems the practical risk is low — but it's worth understanding.

How to certify and avoid mistakes

Submit the PSLF Employment Certification Form (ECF) every year and whenever you change employers. This is how your qualifying payment count gets tracked — don't wait until year ten to certify.

The most common physician mistakes: refinancing federal loans (which permanently forfeits PSLF), sitting in a forbearance that doesn't count, choosing a non-qualifying repayment plan, and never certifying employment. Before any irreversible move, run your numbers to confirm forgiveness is your cheapest path, and pick the right plan with our best repayment plan for physicians guide.

Does PSLF actually pay out? Yes — well over a million borrowers have now had loans forgiven. The scary "low approval rate" headlines mostly reflect applications from people who hadn't yet reached 120 payments, plus paperwork errors. The program works for those who follow the steps.

Which repayment plans keep PSLF payments qualifying

PSLF only counts payments made on a qualifying income-driven plan. That is the piece the 2026 changes touch most, so it is worth being precise. Qualifying plans include the legacy income-driven plans that remain available (such as capped IBR for those who qualify) and the new RAP plan. The Standard 10-year plan technically counts, but its payments are so high that it defeats the purpose — you'd pay the loan off before forgiveness ever arrives. Extended and graduated plans generally do not qualify.

The practical rule for physicians: pick the qualifying plan with the lowest monthly payment you can legitimately claim, because on the PSLF track every dollar you don't pay is a dollar that gets forgiven tax-free. That is the opposite instinct from normal debt payoff, and it is where a good physician student loan calculator earns its keep.

What if some months didn't count? PSLF buyback

Many physicians discover, years in, that some months did not count — often because they sat in a forbearance during training or were briefly on a non-qualifying plan. PSLF buyback lets you retroactively "buy back" certain months of forbearance or deferment by paying what you would have paid on an income-driven plan, so those months count toward your 120. It is a genuine second chance, but it only helps if you were otherwise at a qualifying employer during those months. The takeaway: certify early and often so gaps surface while they are still fixable, not at payment 118.

Consolidation timing and the 2026 deadline

If you hold older loan types (FFEL or Perkins), they must be consolidated into a Direct Consolidation Loan before they can earn PSLF credit. Consolidation used to reset your qualifying-payment count, which made timing critical. Under current rules a weighted-average count is preserved in many cases, but the mechanics changed again for 2026, and there is a June 30, 2026 consolidation deadline tied to reaching certain income-driven plans. If any of your loans are not Direct Loans, confirm the current consolidation rules at studentaid.gov before you act — consolidating at the wrong moment is one of the few PSLF mistakes that is hard to undo.

A resident's PSLF math

Here is why PSLF for doctors explained always starts in training. Picture a resident with a $220,000 balance earning $65,000, headed for a $300,000 attending salary at a nonprofit academic center:

- Residency (years 1–4): income-driven payments of a few hundred dollars a month — roughly 48 qualifying payments made at the cheapest rate of her career.

- Fellowship (years 5–6): still nonprofit, still low income — another ~24 qualifying payments.

- Attending (years 7–10): income-driven payment now capped, the last ~48 payments.

- Payment 120: the remaining balance — frequently well over $100,000 after interest — is forgiven tax-free.

Notice that most of the value came from the cheap training-year payments. A resident who instead sits in forbearance "to deal with it later," or who refinances chasing a lower rate, throws that value away. That is the single most expensive mistake in this entire guide.

What "full-time" means for PSLF

PSLF requires full-time work, but the definition is more generous than physicians assume. Full-time means the greater of 30 hours per week or your employer's definition of full-time. Crucially, if you work for two qualifying part-time employers that together exceed 30 hours, that combination can count — useful for physicians splitting time across academic and VA sites. Vacation and approved leave don't break your status. The month still only counts, however, if you actually make a scheduled payment (or have a $0 income-driven payment) during it.

Married physicians and PSLF

Marriage changes the math in two directions. On the payment side, income-driven plans generally count household income when you file jointly, which can raise your payment; filing separately can lower it, though it carries its own tax cost that must be weighed. On the forgiveness side, PSLF is individual — your spouse's loans and job don't affect whether your loans are forgiven. For dual-physician couples both pursuing PSLF, the interplay of filing status and two income-driven payments is genuinely complex, and it's one of the highest-value things to model rather than guess. See married filing separately and student loans.

PSLF myths, debunked

A few persistent myths keep physicians from a program that would save them six figures:

- "PSLF never actually pays out." False — over a million borrowers have been forgiven. Early denial rates reflected incomplete applications, not a broken program.

- "Residency doesn't count." Usually the opposite — most teaching hospitals qualify, and residency is where the cheapest qualifying payments happen.

- "Forgiveness is taxable." Not for PSLF. PSLF forgiveness is tax-free at the federal level; it's long-term income-driven forgiveness that is taxable.

- "I make too much as an attending to benefit." High income is exactly why the capped payment plus tax-free forgiveness can beat paying the full balance — run the numbers before assuming.

How to submit your ECF, step by step

Certifying employment is the mechanical heart of PSLF, and it's simpler than physicians fear. Once a year (and whenever you change employers), you complete the PSLF Employment Certification Form: you fill in your section, your employer's HR or authorized official signs to confirm your employment dates and hours, and you submit it through the official PSLF Help Tool at studentaid.gov. Your servicer then updates your qualifying-payment count.

Three habits keep it painless. First, certify on a fixed schedule — pick a date, like your work anniversary, so it never slips. Second, keep every signed form; if a servicer ever miscounts, your own records are the fastest fix. Third, re-certify immediately after any job change, before details get hard to reconstruct. The physicians who reach forgiveness smoothly aren't the ones who understood every rule — they're the ones who certified every year and kept the paperwork.

Frequently asked questions

Do doctors qualify for PSLF?

Yes, if they work full-time for a government or 501(c)(3) nonprofit employer on a qualifying income-driven plan and make 120 qualifying Direct Loan payments. Eligibility follows the W-2 employer, not the hospital building.

Is PSLF forgiveness taxable for physicians?

No. PSLF forgiveness is tax-free at the federal level, unlike standard income-driven repayment forgiveness.

Do residency years count toward PSLF for doctors?

Usually yes — most teaching hospitals are nonprofit or government employers, so residency payments typically qualify. Confirm your specific employer and stay on a qualifying plan.

Related guides

Educational estimates, not financial, tax, or legal advice. Program rules change; verify your situation at studentaid.gov and with a qualified advisor. Model your own numbers free at AttendingFi — no login required.