Physician Student Loan Calculator: Free, No Login (2026)

This free physician student loan calculator shows you exactly what your student loans will cost under every repayment path — PSLF, the new RAP plan, capped IBR, and refinancing — modeled on your real numbers, with no login required to see your answer. In about three minutes you'll get one clear, ranked recommendation and see the math behind it.

The short version

- Compares PSLF, RAP, capped IBR, refinancing, and standard — ranked by lifetime cost, not just monthly payment.

- Models the physician income cliff (resident → attending) that generic calculators miss.

- Built on Department of Education, IRS, and HHS rules for 2026.

- No login to see your answer; create a free account only to save it.

- Works for dentists too, including the higher-balance private-practice playbook.

What the physician student loan calculator does

A generic loan calculator tells you a monthly payment. A physician student loan calculator answers the question that actually matters: which repayment path costs you the least over the life of the loan?

It simulates every option against your real trajectory — resident income today, attending income tomorrow — and ranks them by lifetime cost:

- PSLF on an income-driven plan (tax-free forgiveness after 120 qualifying payments)

- The RAP plan (1–10% of total income, forgiveness after 30 years)

- Capped legacy IBR (payment capped at the standard amount)

- Refinancing to a private lender at a lower rate

- Doing nothing / standard repayment

It's built directly on Department of Education, IRS, and HHS rules, so the answer reflects the actual 2026 federal landscape — not a rule of thumb.

How to use it in 3 steps

- Enter your loans — balance and interest rate(s).

- Enter your picture — income now and as an attending, your training, your employer type, and filing status. These are the four inputs that decide your answer.

- Get your ranked plan — the physician student loan calculator returns one clear recommendation, shows every path's total cost, and explains exactly why your plan won.

No account is required to see your answer. You can create a free account afterward to save it and unlock year-by-year modeling.

Why physicians need a specialized calculator

Physician debt behaves differently from typical borrower debt, and a general tool gets it wrong:

- The income cliff. A physician's income multiplies from resident to attending, which changes income-driven payments and the PSLF calculus in ways a flat calculator can't model.

- The employer nuance. PSLF eligibility follows your W-2 employer, not the hospital — a distinction a general tool ignores.

- The forgiveness-vs-refinance fork. For a doctor with a $300k balance, refinancing can be a six-figure mistake. A proper physician student loan calculator will tell a PSLF-eligible doctor not to refinance.

For the strategy behind the numbers, see best student loan repayment plan for physicians and PSLF for doctors explained.

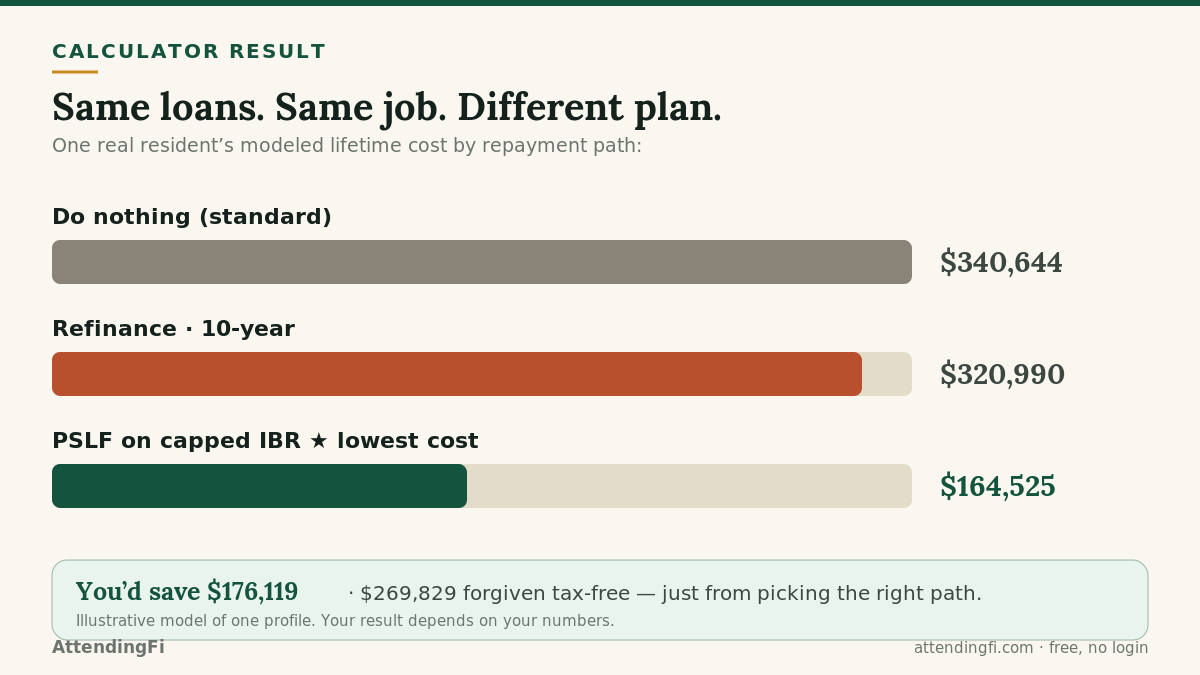

A real example

Here's a real resident's result from the calculator. On the same loans and the same job, the plans diverge sharply:

- Do nothing: $340,644 total paid

- Refinance (10-year): $320,990 total paid

- PSLF on capped IBR (lowest cost): $164,525 total paid

That's $176,119 saved — and $269,829 forgiven tax-free — just from picking the right path. Same loans. Same job. Just the right plan. That gap is exactly what a physician student loan calculator exists to find.

Prefer a single-program view? Try our PSLF calculator, refinance savings calculator, or student loan tax bomb calculator. Always confirm program rules at the U.S. Department of Education's Federal Student Aid site.

What you'll need before you start

The physician student loan calculator returns a better answer when you feed it real numbers instead of guesses. Gather these first — most are on your studentaid.gov dashboard or a recent statement:

- Total federal balance and weighted interest rate. If you have several loans, the tool blends them; you don't need every line item.

- Current income (resident/fellow) and expected attending income. The jump between them is what makes physician math unique.

- Months left in training. This tells the model how long your cheap, forgiveness-friendly payments last.

- Employer type — nonprofit/government or for-profit — which decides whether PSLF is even on the table.

- Filing status and spouse income if married, since that changes income-driven payments.

None of this requires an account, and nothing is shared. You enter it, the physician student loan calculator runs the scenarios, and you see the ranked result.

How the model works (and its assumptions)

Under the hood, the tool projects each repayment path month by month across your whole career, not just the current year. It applies the current federal formulas — income-driven payment percentages, the IBR payment cap, RAP's tiers and interest waiver, the PSLF 120-payment rule, and the tax treatment of each kind of forgiveness — then totals the lifetime cost of every path and ranks them.

A few assumptions are worth knowing, because transparency is the point: it models a reasonable income-growth trajectory from resident to attending, uses current-year federal poverty guidelines and tax parameters, and treats PSLF forgiveness as tax-free and long-term income-driven forgiveness as taxable. Real life varies — raises, moves, and rule changes all shift the numbers — which is exactly why the honest use of any physician student loan calculator is to re-run it whenever something changes, not to treat one result as permanent.

For residents, fellows, attendings — and dentists

The right output looks different at each stage:

- Residents and fellows mostly want confirmation that they're on the cheapest PSLF-qualifying plan and not wasting months in forbearance.

- New attendings face the highest-stakes decision the tool exists for: with income about to multiply, is it finish PSLF, switch plans, or refinance? Run it the week your contract is signed.

- Established attendings use it to sanity-check a plan they set years ago against the 2026 rules — and to catch a recommendation that has quietly changed.

- Dentists get the same engine with the higher-balance, mostly-private-practice reality baked in, where refinancing and capped IBR win more often than they do for MDs.

Whatever your stage, the value is the same: one clear, ranked answer with the math shown, so a six-figure decision stops being a guess.

Why lifetime cost beats monthly payment

The most common way physicians get their loan decision wrong is by optimizing the monthly payment instead of the total. A plan with a low monthly payment can be the most expensive over time, and a higher monthly payment can be the cheapest — it depends on interest, forgiveness, and how long you pay. That's the whole reason a physician student loan calculator ranks by lifetime cost: the number that actually leaves your pocket across the life of the loan, including any tax on forgiveness.

Consider the earlier example — the PSLF path had a modest monthly payment and a low lifetime cost, while "do nothing" had a manageable-looking payment but the highest total of all. Monthly payment tells you what fits your budget this month; lifetime cost tells you which decision is actually right. A good calculator shows you both, but ranks on the one that matters.

How the calculator stays accurate

Federal student loan rules change — sometimes several times a year, as 2026 proved. A physician student loan calculator is only as good as the rules it encodes, so this one is built directly on primary sources: Department of Education repayment and PSLF rules, IRS tax treatment of forgiveness, and HHS poverty guidelines that drive income-driven payments. When the rules shift — SAVE winding down, RAP launching, IBR changes — the model is updated to match, so the answer reflects the current landscape rather than last year's.

That said, no model replaces personalized advice for a truly complex situation (multiple degrees, a business, unusual loan types). The calculator's job is to get you a correct, transparent baseline in three minutes and flag when your decision is close enough to warrant a second look. For everything it shows, the underlying math is visible — because a recommendation you can't inspect isn't one you should trust with six figures.

Questions the calculator settles for you

A physician student loan calculator earns its place by answering the specific, high-stakes questions that keep doctors up at night — with numbers instead of opinions:

- "Should I refinance, or will I lose forgiveness?" It compares your refinance savings against your projected PSLF forgiveness and tells you which is larger — the single most consequential number in your financial life.

- "Is PSLF actually worth staying at a nonprofit for?" It quantifies the forgiveness, so "I like this job" and "this job is worth $X in forgiveness" become two separate, clear-eyed decisions.

- "RAP or capped IBR?" It models both against your attending income and shows which keeps more of your balance for forgiveness.

- "How bad is the tax bomb?" For non-PSLF forgiveness, it estimates the future taxable amount so you can save for it.

- "Did my answer change?" Re-running after a raise, a move, or a rule change catches a recommendation that has quietly flipped — before it costs you.

Each of these is worth tens of thousands of dollars to get right, and each depends on inputs unique to you. That's the case for modeling your own numbers rather than trusting a headline — and it's why the tool is free and needs no login to give you the answer.

Free, no login — and why

Most physician student loan calculators either oversimplify the math or gate the real answer behind a signup, an email, or a sales call with an advisor who earns a commission on refinancing. That model has an obvious conflict: a tool paid by lenders has a reason to nudge you toward refinancing, which is exactly the move that can cost a PSLF-eligible doctor six figures. This calculator takes the opposite stance — you see your ranked result immediately, for free, with no account required, and the tool is just as willing to tell you not to refinance as to do it. You can create a free account afterward if you want to save your plan, track PSLF progress, or model year by year, but the core answer is yours to see up front. When a decision is worth six figures, the least you should expect is to see the math before anyone asks for your email.

Frequently asked questions

Is the physician student loan calculator free?

Yes — it's completely free and requires no login to see your answer. Create a free account afterward only if you want to save your plan.

What does the physician student loan calculator compare?

PSLF, the new RAP plan, capped IBR, refinancing, and standard repayment — ranked by what each costs you over the life of the loan on your exact numbers.

Does it work for dentists?

Yes. The calculator models dentists as well as physicians, including the higher-balance, mostly-private-practice playbook that changes the math.

Is it accurate for 2026 rules?

It's built on current Department of Education, IRS, and HHS guidelines, including the 2026 RAP plan and IBR changes. Always verify your specifics at studentaid.gov.

Related guides

Educational estimates, not financial, tax, or legal advice. Program rules change; verify your situation at studentaid.gov and with a qualified advisor. Model your own numbers free at AttendingFi — no login required.