How to Pay Off Medical School Loans Fast: 7 Steps

Learning how to pay off medical school loans is really about one choice: whether to pay them off aggressively or have them forgiven — because for many physicians, chasing forgiveness is mathematically the faster path to zero out of pocket. This 7-step guide shows you how to decide, in 2026, with a median medical school debt around $200,000 on the line.

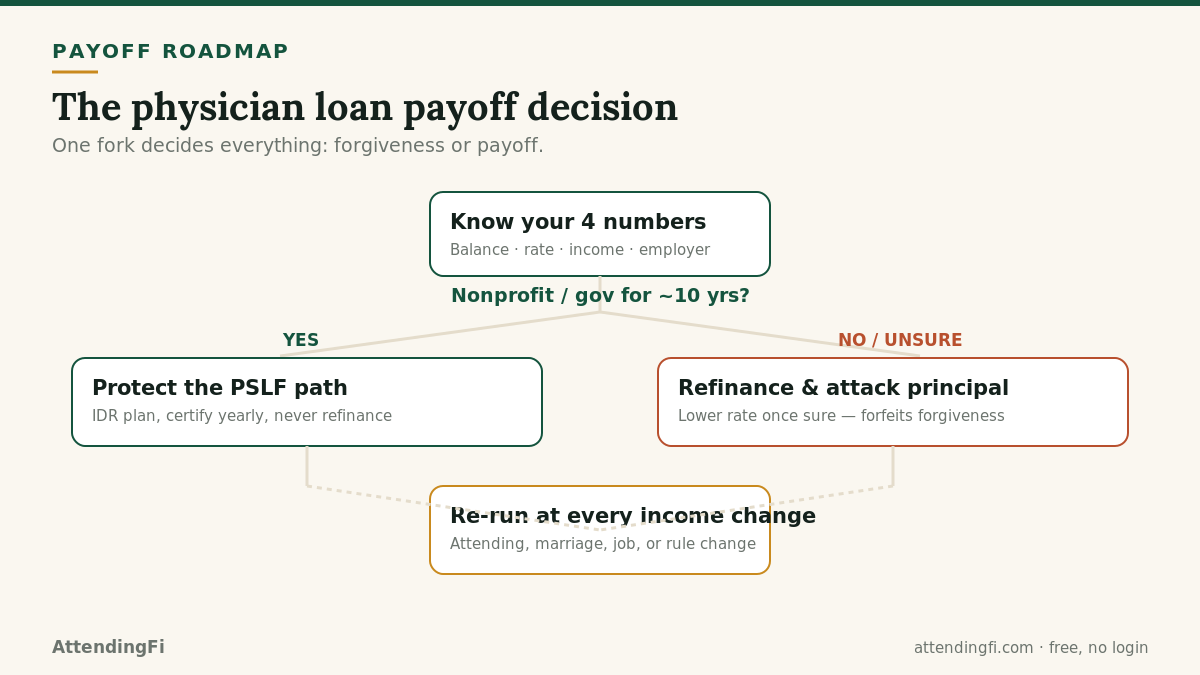

The short version

- "Pay it off fast" is not automatically right — overpaying a forgiven balance costs six figures.

- First fork: will you work nonprofit/government for ~10 years? Yes → forgiveness; No → payoff.

- On the payoff path, refinancing to a lower rate is usually fastest — but it's permanent.

- Married on an income-driven plan? Filing separately can slash your payment.

- Re-run the plan at every income change — the math flips from resident to attending.

How to pay off medical school loans starts with one decision

The first thing to accept about how to pay off medical school loans is that "pay it off fast" is not automatically the right goal. Aggressively paying down a balance headed for tax-free forgiveness can cost you six figures. Before any payment strategy, you settle a single question: forgiveness or payoff. The seven steps below walk you through it.

Step 1: Know your exact numbers

You can't plan how to pay off medical school loans without four numbers: your total balance, your interest rate(s), your income now and as an attending, and your employer type. Per the AAMC, the median medical school debt is roughly $200,000, and the right strategy for a $150k balance differs sharply from a $400k balance.

Step 2: Decide — forgiveness or payoff?

This is the fork that determines everything. Ask: Will you work for a nonprofit or government employer for about ten years?

- Yes → the forgiveness path (PSLF) is usually the cheapest way to reach zero. You'll pay income-driven amounts for 120 months and have the rest forgiven tax-free.

- No / unsure → the payoff path, where you minimize total interest and clear the balance yourself.

There is no honest way to answer "how to pay off medical school loans" without settling this first.

Step 3: If forgiveness, protect your PSLF path

On the forgiveness path, the goal isn't to pay more — it's to make every payment qualify while paying as little as legally possible. Get on an income-driven plan in residency, certify employment yearly, and never refinance (which permanently kills PSLF). See PSLF for doctors explained.

Counterintuitively, on this path, not rushing to pay off medical school loans is the optimal move — extra dollars thrown at a forgiven balance are dollars lost.

Step 4: If payoff, choose payoff vs. refinance

If forgiveness isn't in your future, the fastest way to pay off medical school loans is usually to refinance to a lower rate and then attack the principal. Refinancing is permanent and forfeits federal protections, so only do it once you're certain — but for a private-practice physician with strong cash flow, a lower rate plus aggressive payments can shave years and tens of thousands in interest.

Compare rates and run the break-even with our refinance savings calculator and should I refinance guide.

Step 5: Optimize your filing status

For married physicians on income-driven plans, married filing separately can dramatically lower your monthly payment (and therefore raise your eventual forgiveness) when one spouse earns much more than the other. It's a calculation, not a rule of thumb — the tax cost of filing separately must be weighed against the loan savings. See our married filing separately guide.

Step 6: Avoid the six-figure mistakes

The most expensive errors when figuring out how to pay off medical school loans:

- Refinancing while forgiveness-eligible — a permanent, often six-figure mistake.

- Overpaying a balance headed for forgiveness.

- Consolidating at the wrong time and resetting your PSLF count.

- Sitting in a forbearance that doesn't count toward forgiveness.

- Ignoring the tax treatment — PSLF forgiveness is tax-free, but standard income-driven forgiveness is taxable, so plan for that "tax bomb" with our tax bomb calculator.

Step 7: Re-run the plan at every income change

The best plan for how to pay off medical school loans is not static. When your income jumps from resident to attending, when you marry, when you change employers, or when the federal rules change (as they did for 2026 with the new RAP plan and the June 30 consolidation deadline), the math can flip. Re-run it — free, no login — at AttendingFi, or start with the best repayment plan for physicians.

A worked example: $250,000, two paths to zero

Numbers make the forgiveness-vs-payoff choice concrete. Take a physician finishing training with a $250,000 balance at 7% and a $300,000 attending salary. How to pay off medical school loans depends entirely on where she works.

- Nonprofit hospital (PSLF path): she stays on capped IBR, makes low income-driven payments through training and capped payments as an attending, and reaches forgiveness at 120 payments. Her total out of pocket is often in the low-to-mid $100,000s, with the remaining balance forgiven tax-free. Paying extra here would only shrink the forgiven amount — a direct loss.

- Private practice (payoff path): forgiveness is off the table, so she refinances from 7% to a lower private rate and throws her strong attending cash flow at the principal. She clears the balance in roughly 5–7 years, paying the full principal plus reduced interest — more out of pocket than the PSLF physician, but the fastest honest route to zero when forgiveness isn't available.

Same balance, same interest rate, same salary — and the cheapest strategy differs by six figures based on one variable: the employer. This is why "just pay it off fast" is dangerous advice for doctors.

What flips the answer

A handful of variables change how to pay off medical school loans more than anything else. Watch these:

- Employer type — nonprofit/government unlocks tax-free PSLF; for-profit rules it out. This is the single biggest lever.

- Balance-to-income ratio — a debt roughly equal to or larger than income favors forgiveness; a small balance relative to a high income favors fast payoff.

- Filing status — for married physicians on income-driven plans, filing separately can lower payments enough to change the whole calculus.

- Interest rate — a high fixed rate makes refinancing more attractive on the payoff path (but never on the forgiveness path).

- Time already banked — if you're 90 payments into PSLF, finishing is almost always right, even if you later move private.

Because these interact, the reliable way to know how to pay off medical school loans in your case is to model all of them at once rather than reason about them one at a time.

When to refinance (and when never to)

If you land firmly on the payoff path, refinance timing matters. Rates you qualify for improve once you're an attending with a signed contract and steady income, so many physicians refinance shortly after starting their first attending job rather than during residency. But the rule that overrides all timing: never refinance federal loans while forgiveness is realistically in reach. Refinancing is permanent and forfeits PSLF, income-driven plans, and every federal protection. If there is any chance you'll work for a nonprofit, keep your loans federal until you're certain — run the refinance savings calculator against your forgiveness estimate first.

Don't forget the tax bomb

There is one more variable that quietly changes how to pay off medical school loans on the non-PSLF forgiveness path. If you stay on an income-driven plan for 20–30 years without qualifying for PSLF, the balance forgiven at the end is treated as taxable income in that year — a lump-sum "tax bomb" that can run into six figures. PSLF forgiveness is tax-free; long-term income-driven forgiveness is not. For a private-practice physician who can't refinance affordably and rides an income-driven plan to forgiveness, the right move is to set aside a sinking fund for that future tax bill. Estimate it early with the student loan tax bomb calculator so it's a planned expense, not a surprise.

Consolidate the right loans, at the right time

Before any strategy works, your loans have to be eligible for it. Only federal Direct Loans qualify for PSLF and the income-driven plans; older FFEL or Perkins loans must first be consolidated into a Direct Consolidation Loan. But timing matters: consolidating can affect your qualifying-payment history, and the 2026 rules added a June 30, 2026 deadline tied to reaching certain plans. The safe sequence is to confirm exactly which of your loans are Direct, check the current consolidation rules at studentaid.gov, and model the consequence before you consolidate — because unlike a monthly payment, a mistimed consolidation is hard to reverse.

A note for dentists and high-balance borrowers

Dentists face the same framework with the dial turned up. Dental school debt frequently runs higher than medical school debt — balances north of $300,000 are common — and most dentists head into private practice rather than nonprofit employment, which takes PSLF off the table for many. That combination pushes the answer toward the payoff path more often than for physicians: refinance to a lower rate once income is stable, then attack the principal. But the same guardrail applies — associates who spend early-career years at a nonprofit or public clinic may still bank PSLF-qualifying months, so confirm your employer before assuming forgiveness is unavailable. The higher the balance, the more a wrong turn costs, which is precisely why modeling beats rules of thumb here.

The order of operations

Put the seven steps together and how to pay off medical school loans becomes a clean sequence: (1) gather your four numbers, (2) settle forgiveness vs. payoff based on your employer, (3) on the forgiveness path, get on the cheapest qualifying plan and certify yearly, (4) on the payoff path, refinance once you're sure and attack principal, (5) optimize filing status if married, (6) plan for the tax bomb if you're on non-PSLF forgiveness, and (7) re-run everything whenever your life changes. Follow that order and the six-figure mistakes take care of themselves.

Frequently asked questions

What's the fastest way to pay off medical school loans?

For physicians headed to private practice, refinancing to a lower rate and attacking the principal is usually fastest. For those at nonprofit/government employers, PSLF forgiveness often reaches zero out-of-pocket faster than paying the full balance.

Should I pay off medical school loans or go for forgiveness?

It depends on your employer and balance. If you'll work ~10 years at a qualifying nonprofit/government employer, forgiveness is usually cheaper; if you're private practice, aggressive payoff or refinancing typically wins.

How long does it take to pay off medical school loans?

Anywhere from ~5 years (aggressive payoff/refinance on a high income) to 10 years for PSLF forgiveness, to 20–30 years on income-driven plans without forgiveness. Your plan choice sets the timeline.

Related guides

Educational estimates, not financial, tax, or legal advice. Program rules change; verify your situation at studentaid.gov and with a qualified advisor. Model your own numbers free at AttendingFi — no login required.